The 26% factor

Welcome back. This is Episode Six of AlphaFrame, and it may be the most important half hour in the whole series — because today we talk about tax. Not the exciting part, I know. But here is the honest truth for us as euro-based Italian retail investors: a strategy is not what it earns on paper. It is what it keeps after the Italian State takes its share. And in Italy, that share on financial gains is twenty-six percent — a flat rate applied to your capital gain, the profit between what you sold at and what you bought at. Twenty-six cents of every euro of gain, gone.

So let me set the frame for the next thirty minutes. A backtest can look brilliant. It can show a beautiful curve, big returns, all in gross dollars, run on foreign data. And that same strategy, once we translate it into euros and subtract the twenty-six percent, can turn out to be mediocre — sometimes barely better than doing nothing. The gross number seduces; the net number decides.

Most of the strategies you see marketed online quietly ignore this. They report gross, in dollars, before any tax. We will not do that. In this series we treat net-of-tax as the only honest number — the only figure worth comparing.

Today we will do three things. First, we will measure how much the twenty-six percent quietly drags down each of our engines. Second, we will see why that drag compounds over the years — why it grows. Third, we will show how we build around it, engine by engine, so the edge that survives tax is real.

One anchor before we start, and we will repeat it often: this is the standard twenty-six percent regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista. Let us begin.

The engines at a glance

Before we open the tax question, let's put our engines back on the table, quickly, so we all share the same picture. We run three families of models. The first is our main research engine: LSTM networks with attention over ETFs. Think of it as a system that reads the recent history of a set of ETFs and decides how much weight each one deserves. The second family is our candidates: models we are testing, that have shown promise but have not earned a place among the main models yet. The third family is the mechanical engines: rule-based approaches, momentum and regime signals, no learning, just transparent instructions we can read line by line. Three families, three different ways of deciding what to hold and when to change it. In the earlier episodes we compared them mostly on gross returns, the numbers before the State takes its share. And on gross numbers, they tell one story. But here is the turn this whole episode makes: today we are not adding a fourth engine. Today we are sliding a layer underneath all three of them. That layer is Italian taxation, the 26 percent that applies to most financial gains for a private investor. It does not care which engine produced the gain. It sits under the deep learning engine, under the candidates, under the mechanical rules, and it quietly changes every verdict we reached. A model that looks best before tax may not be best after tax. In the next slides we will see, with real measured numbers, how large that change is. Just remember the frame: this is the standard 26 percent regime amministrato with cost-basis; rules change and individual situations differ, so consult a commercialista.

Net-of-tax is the only number that matters

Here is the rule that governs this entire episode, and it is simple: the investor keeps the net, not the gross. When we say "gross return," we mean the return before any tax is taken. That is a marketing number. What actually lands in your account is what is left after the Italian State takes its share. And in Italy, on financial gains, that share is the imposta sul capital gain — the capital-gains tax — at a rate of 26% on realised gains. "Realised" is the key word: the tax is due when you actually sell at a profit, not while the position is only rising on paper. So a gain you never sell is not yet taxed; the day you sell it, 26% of that profit goes to the State. Now think about what this does to every comparison. When we compare our strategy against the index, or against a rival strategy, the only honest comparison is net of that 26%. A gross number that ignores tax is not describing your experience as an Italian investor — it is describing a world you do not live in. And here is the uncomfortable part: most published backtests, most marketed track records, quote gross returns, and very often in a foreign currency, typically dollars. That figure is close to irrelevant to what you, in euro, under Italian rules, actually bank at the end. It flatters the strategy and it flatters the seller. So we make ourselves a promise for this whole episode: we judge everything net. Every engine, every comparison, every headline number you will see from slide four onward is after the 26% has been subtracted. Remember: this is the standard 26% regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista. Next, we measure exactly how heavy that drag is, engine by engine.

The measured drag, per engine

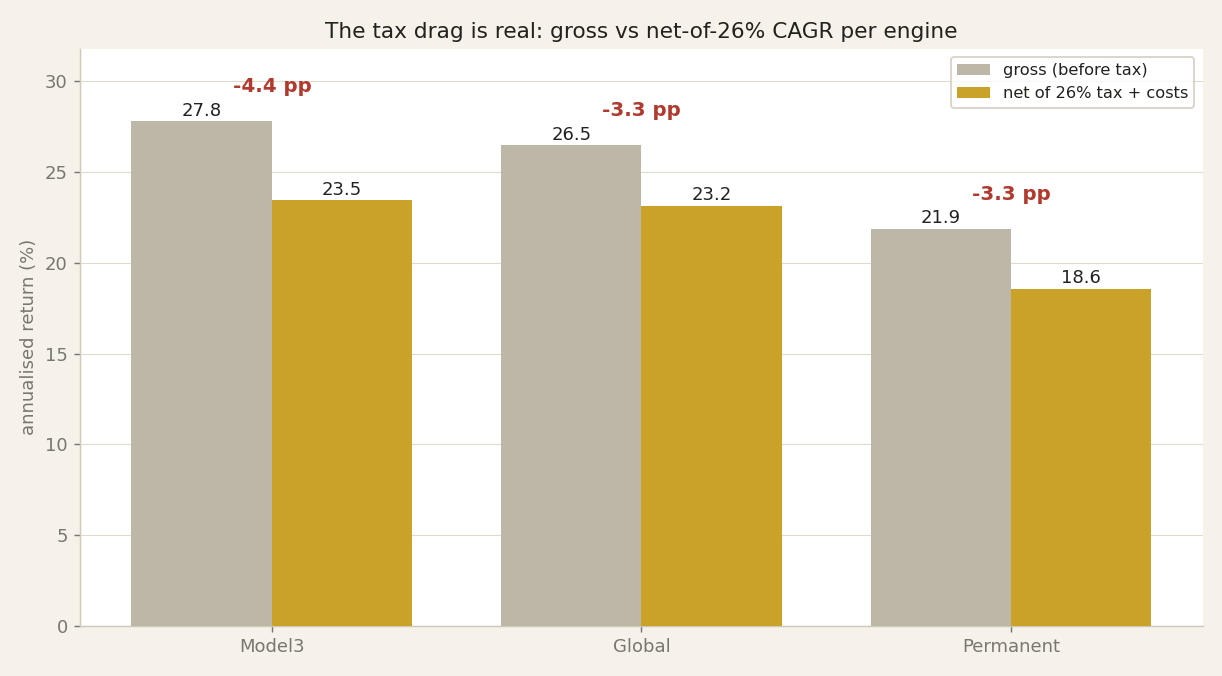

Look at this chart. For each of our three main research engines, the left bar is the gross return — before any tax — and the right bar is what actually reaches us, after the Italian tax on financial gains takes its share. Let me define the return measure first: CAGR, the compound annual growth rate, is simply the steady yearly rate that turns the starting amount into the ending amount over the whole period. Now the numbers, measured with cost-basis tracking, meaning we follow the real purchase price of each position and tax only the actual realised gain. Our first engine — the LSTM networks with attention over ETFs — goes from 27.8 percent gross to 23.5 percent net. That is a drag of 4.35 percentage points every year. The Global engine goes from 26.5 to 23.2 percent, a drag of 3.32 points. The Permanent engine goes from 21.9 to 18.6 percent, a drag of 3.30 points. So across all three, the tax quietly removes between roughly 3.3 and 4.4 percentage points of annual return. This is not a fee we can shop around for. It is a toll, paid every single year, and the faster-trading engine pays the most because it realises gains more often. Notice the pattern already: the engine with the highest gross return also carries the heaviest tax drag. That is the tension we will unpack in the next slides — because a percentage point lost each year does not just subtract once, it compounds. And to be clear about the framework: this is the standard 26 percent regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista.

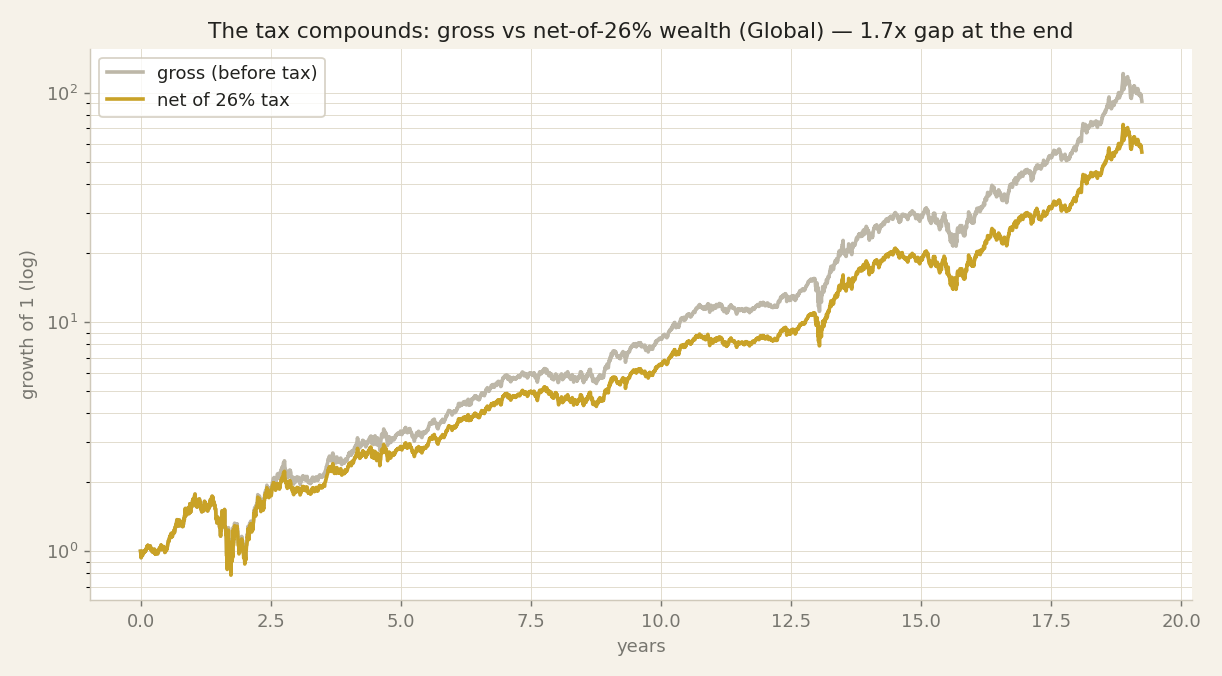

The drag compounds

In the previous slide we saw the drag per engine: three to four percentage points a year taken by tax. Now here is the part that hurts. That drag is not linear. It compounds. Look at this chart. One line is the gross wealth curve — what one engine would have built before tax. The other line is the net wealth curve — what actually lands in your pocket after the 26% tax on gains. At the start, over on the left, the two lines sit almost on top of each other. A three or four point drag in year one looks like a rounding error. But watch them walk apart. Each year the tax is taken off a base that would otherwise have kept compounding. The money handed to the taxman in year two is money that cannot grow in years three, four, five, all the way out. By the right-hand edge, after the full roughly seventeen-year history, the two curves have separated dramatically — a wide, growing gap between what the engine earned and what you keep. That is the whole lesson of this episode in one picture: a small annual tax drag becomes a large terminal wealth gap. The size of the gap is driven by time and by how often gains are realised. And this is exactly why turnover — trading that forces you to realise gains and pay the tax now rather than letting them ride — is so expensive. Every unnecessary trade drags the net line further below the gross line, and the damage compounds for the rest of the horizon. Remember, this is the standard 26% regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista. In the next slide we open up where this tax actually sits: the two buckets, redditi di capitale versus redditi diversi.

Two buckets: redditi di capitale vs diversi

Now we hit the Italian quirk that trips almost everyone, and it lives in this table. The tax office does not treat all your gains and losses the same way. It sorts them into two buckets. First term: "redditi di capitale" — capital income. Second term: "redditi diversi" — literally "other income", the bucket that holds trading gains and losses on most instruments. The names sound like paperwork. The difference costs real money.

Read the table with me. When your ETF or fund — in the law, an OICR — makes a capital gain, that gain is redditi di capitale, taxed at twenty-six percent, and here is the trap: it cannot be reduced by any capital loss. Not this year's, not a stored one. But when the same ETF makes a capital loss, that loss is redditi diversi — it drops into your loss ledger. Now look at single stocks, bonds, ETCs and ETNs, and derivatives. For all of these, both the gains and the losses are redditi diversi. So a gain on a single stock CAN be offset by a prior loss. A gain on an ETF cannot.

That is the asymmetry, and I want it burned in: an ETF gain can never be sheltered by a loss — not by an ETF loss, not by any loss. The loss goes in one bucket; the gain sits in another the ledger cannot reach.

This is the standard twenty-six percent regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista.

Keep this two-bucket map in your head, because next we open that loss ledger itself — the "zainetto fiscale", the tax backpack — and see exactly how a stored loss lives, and how it can quietly expire.

The loss ledger — the zainetto fiscale

So the tax bites. Does Italian law give us anything back? It does — one thing. It's called the "zainetto fiscale", the tax loss backpack. Let's define it plainly. When we sell an ETF for less than we paid, we realise a loss — a "minusvalenza". That loss doesn't vanish. It goes into a ledger, and it can be used to offset future gains, cancelling the 26% we would otherwise owe on them. That's the backpack: a store of past losses waiting for future gains.

But there are hard rules, and we model every one of them exactly. Rule one: the offset only works forward in time. A loss can cover a gain realised after it, never before. Rule two: each loss expires. It lives only until the 31st of December of the fourth year after the loss — then it's gone, worthless. Rule three: when a gain arrives, we spend the oldest losses first.

Now the sting, and this is the whole point of the episode. Losses from ETFs go into the backpack — they count as "redditi diversi", the "other income" bucket. But gains from ETFs and funds are "redditi di capitale", capital income — a separate bucket. And a capital-income gain can never reach into the backpack. So if we hold only ETFs, losses fill the backpack, gains can't empty it, and after four years the whole thing simply expires. Full, and useless.

We built this into our engine — a function that applies the ledger chronologically, oldest-first, with the four-year expiry — so every net-of-tax number you've seen respects these rules.

Next slide, we walk a real ledger through year by year, so you can watch a loss expire unused.

Remember: this is the standard 26% regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista.

The zainetto, worked

Let's make the loss ledger — the zainetto fiscale — concrete with one toy example. Picture five columns: year, event, taxable, tax, and ledger left. In Year 1 we sell a single stock at a loss of 1,000 euros. Nothing is taxable, no tax is due, and 1,000 euros of losses enter the ledger. Remember the clock we mentioned: this loss expires at the end of Year 5, so we have four full years to use it. In Year 2 we realise a 400-euro gain on a stock. That gain is a reddito diverso — a capital gain of the "miscellaneous income" type — so the ledger can absorb it. Taxable becomes zero, tax is zero, and the ledger falls to 600 euros. So far the system works exactly as we hoped. Now Year 3, the punchline. We realise a 700-euro gain on an ETF. An ETF gain is a reddito di capitale — "income from capital" — and this bucket cannot be offset by the ledger at all. So the full 700 euros is taxable, we pay 26 percent, that is 182 euros of tax, and the ledger stays untouched at 600. We paid full tax with a loss sitting right there, unused. Then Years 4 and 5 pass with no realisations, and in Year 6 the remaining 600 euros of losses expire — gone, worth nothing. That single table is the whole lesson: an ETF gain pays full tax even while a loss waits in the ledger, because the two live in different buckets. This is why, in the next slide, we look at why deliberately harvesting losses on ETFs simply does not help. Remember: this is the standard 26 percent regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista.

Tax-loss harvesting: useless on ETFs

Now let me kill a myth you have almost certainly read on some finance blog. It is called tax-loss harvesting, or TLH: deliberately selling something at a loss to create a realised loss that shelters a gain you owe tax on. It sounds clever. On an ETF-only portfolio, it does nothing. Here is why, and look at the table while I say it. Under Italian rules gains from an ETF are redditi di capitale — literally income from capital, taxed at the source at twenty-six percent, and by law they cannot be reduced by any realised loss. A loss you harvest goes into a completely different drawer, the redditi diversi drawer — other income, mainly capital gains on single stocks. So if you hold only ETFs, the loss you carefully realise fills a ledger that your ETF gains are never allowed to empty. You paid real transaction costs, you added turnover, and you sheltered exactly nothing. The table makes it blunt. Book type: ETFs only — does TLH help? No — because gains and losses sit in two separate buckets that cannot meet. Book type: single stocks, or other redditi diversi — does TLH help? Potentially yes — because there gains and losses share the same bucket and can offset. So the honest rule is simple. If you hold ETFs, forget tax-loss harvesting; it is not a lever you have. On single stocks it genuinely can add value, but it is technical and error-prone, so it needs a commercialista — an accountant — to confirm it in writing before you act. This is the standard twenty-six percent regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista. Next we turn to the cost you can actually control: turnover, and why every trade carries a tax bill.

Turnover is a tax cost

So far we've measured the drag and watched it compound. Now let's connect it to how a strategy is actually built, because turnover is where the tax bill is born. Turnover is the share of the portfolio you rotate in a year: one hundred per cent means that, over twelve months, you sold and rebought the equivalent of the whole portfolio. Here's the mechanism. Every time a rebalance sells a winner, it realises a capital gain — a gain you actually cash in when you sell — and a realised gain triggers the twenty-six per cent right now. Not on paper, not at the end: now, this year, and again next year. A buy-and-hold investor does the opposite: by not selling, they defer that twenty-six per cent to the very end. The tax not yet paid stays invested and keeps compounding for them — effectively an interest-free loan from the State. So the same tax rate, paid early and often versus paid once at the end, produces very different outcomes. This reframes the whole idea of turnover. We usually think of turnover as a trading cost — the spread, the commission. That's real, but it's the small part. The larger part is a tax-timing cost: high turnover drags tax forward, year after year, and every euro of tax paid today is a euro that stops compounding forever. Here is the proof from our own numbers. Take our top two models. Gross, they were basically tied: twenty-seven point eight against twenty-seven point seven. Net, the ranking flipped — twenty-three point four against twenty-three point seven. Why? The gross winner rotated more, so its drag was four point four points against four. Same gross return, different net return, purely from turnover. This is the standard twenty-six per cent regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista. Next, we'll see how our no-trade band turns this insight into a tool.

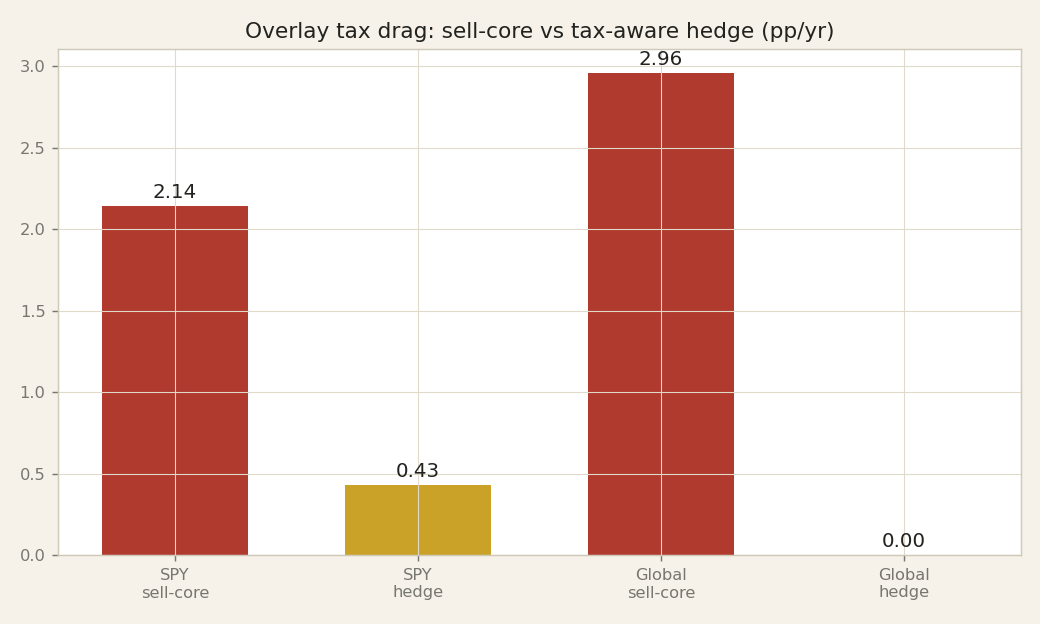

The no-trade band is a tax tool

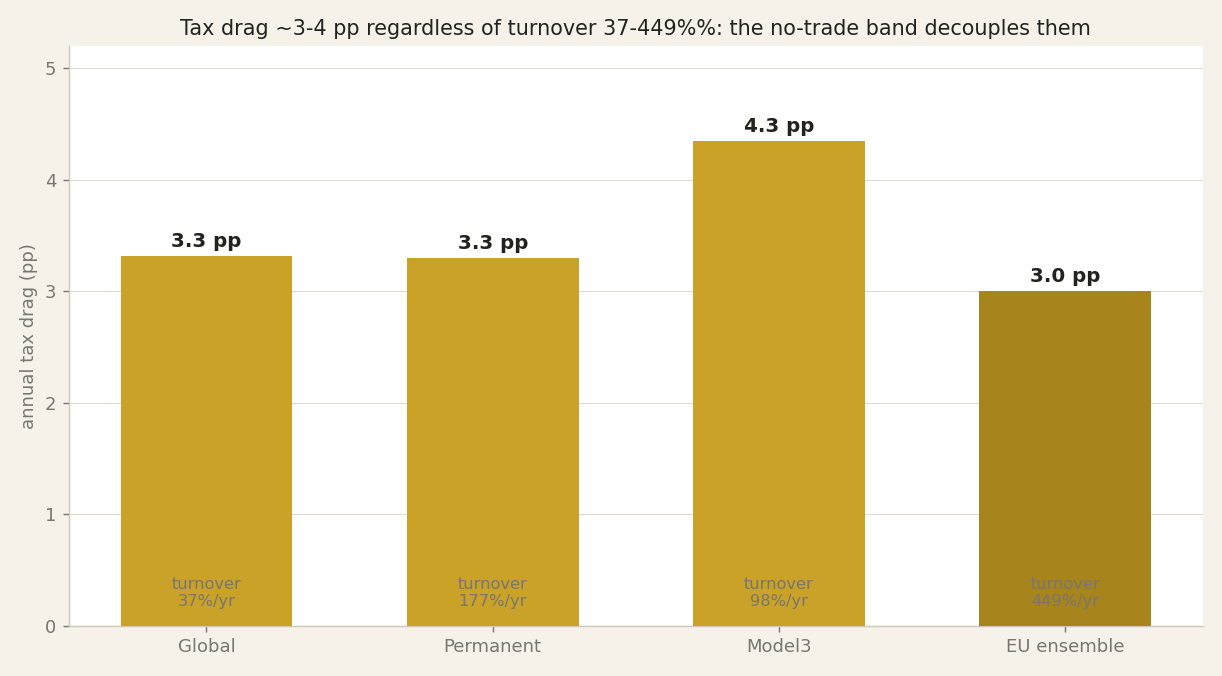

So far we've treated tax as something that happens to us after the fact. On this slide I want to show you a design choice that fights back, quietly, inside the engine itself. Our allocation filter has what we call a no-trade band: we only rebalance a position when the asset moves by at least fifteen percent away from its target weight. If it drifts less than that, we leave it alone. We originally built this to cut noise trading — to stop the model reacting to every small wobble. But it turns out to do a second job for free, and that job is fiscal. Every time we sell to rebalance, we realise a gain or a loss — "realise" meaning we actually crystallise it, so the tax becomes due. Fewer rebalances mean fewer realisations, and fewer realisations mean less tax paid along the way. Look at the chart. The European ensemble — our combination of LSTM networks with attention over ETFs plus the defensive component — runs at roughly four hundred and forty-nine percent annual turnover. That sounds enormous. Yet its net-of-tax drag is only about three percentage points. How? Because the band suppresses the small trades that would each trigger a taxable event, and the defensive leg realises very little gain in the first place. Without the band, that drag would be materially worse — more churn, more crystallised gains, more tax leaking out every year. The lesson: a rule built for signal quality is also a tax instrument. Same band, two benefits. Next slide, we compare ETFs against single stocks on exactly this tax dimension. Remember: this is the standard twenty-six percent regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista.

ETF vs single stocks, on tax

Now put ETFs and single stocks side by side, purely on tax. Look at the table. First row, simplicity: an ETF gives you one diversified instrument; a book of single stocks means picking, weighting, and watching each name yourself. Second row, the tax bucket. Remember the two buckets from earlier: redditi di capitale, capital income, and redditi diversi, other income. An ETF gain falls into redditi di capitale, which cannot be offset against losses. But a single-stock gain and a single-stock loss both fall into redditi diversi, and inside that bucket losses do offset gains. So the third row, your loss ledger, the zainetto fiscale: on an ETF-only book, an ETF loss is essentially wasted, it goes into the ledger but nothing feeds it back out, because your future ETF gains are the wrong bucket. On single stocks the offset actually works. Fourth row, the rate is the same for both: 26 percent, with the 12.5 percent rate applying only to the white-list government-bond portion inside a fund. Fifth row, the cost: single stocks add concentration risk and real effort; the ETF spares you both. Here is the honest, often-ignored asymmetry: the tax code quietly rewards the stock-picker with an offset the ETF holder never gets. That is a structural feature, not an opinion. It is not a reason to abandon diversification and start picking stocks, and it is not us telling you to harvest losses. It is context for reading net-of-tax numbers correctly. And remember: this is the standard 26 percent regime amministrato with cost-basis; rules change and individual situations differ, so consult a commercialista. Next we look at a subtler trap: the foreign backtest that quietly ignores Italian tax.

The foreign-backtest trap

We just saw the drag compound. Now the trap it sets for you as a reader. Almost every strategy marketed to us was measured somewhere else, under someone else's rules. Take a US strategy advertised at, say, fifteen percent a year. That headline is gross — before any tax — and it is in dollars. Two things sit between that number and what would actually reach a Euro investor. First, our tax: the standard twenty-six percent on realised gains, which on our own five models cost between three and four-point-four percentage points a year — a drag that only grows as it compounds. Second, the currency: fifteen percent in dollars is not fifteen percent in euros, because the EUR/USD exchange rate moves, and over a decade it can add or subtract several points either way. Put both together and that advertised fifteen can shrink to a fraction of itself, or disappear entirely. As a fixed reference: the US equity index over our common window returned ten-point-three percent gross in euros — and that is before your tax. We have seen this pattern again and again in our own lab: gross-in-dollars flatters; net-in-euros is the truth, and the truth is a smaller, honest number. So the rule is blunt. Never trust a backtest that has not been localised to your tax and your currency. A result validated gross, in dollars, is simply not a result validated for you. Ask two questions of any headline: is it net of the twenty-six percent, and is it in euros? If the answer to either is no, the number is not yours to spend. And remember — this is the standard twenty-six-percent regime amministrato with cost-basis; rules change and individual situations differ, so consult a commercialista. Next, we turn from foreign numbers to a cost you control at home: turnover.

What we do about it

So what do we actually do about a tax that costs us three to four-point-four points a year? We do four concrete things, and they all live inside the design, not in a footnote. First: we optimise and select net of the twenty-six per cent. Every model that survives our review has to win on net-of-tax numbers — the distribution of what an Italian investor keeps after the twenty-six per cent capital-gains tax and after costs. The gate never reads the gross figure. If a strategy only wins gross, for us it does not exist. Second: we keep a no-trade band. That is a deliberate rule that lets a position drift within a range before we rebalance, so we do not sell — and do not realise a gain, and pay the twenty-six per cent — unless the move is big enough to be worth it. Less selling means tax deferred, and deferred tax keeps compounding for you. Third: we report net, in euros, and we never promise gross. The number we put on screen is the number you would actually keep. Fourth, and this is the mindset that ties it together: a strategy that wins gross but loses net is, for a real Italian investor, a losing strategy — full stop. We treat it as one. The tax is not an afterthought we subtract at the end; it sits inside the objective we optimise from the start. And to be clear, this is the standard twenty-six per cent regime amministrato with cost-basis accounting; rules change and individual situations differ — consult a commercialista. In the next slide, the honest limits: what this discipline still cannot fix.

Honest limits

Before we close, let me be honest about what our numbers do and do not capture. Everything you have seen models one specific setup: the standard regime amministrato — the arrangement where your Italian broker withholds the 26 percent tax for you, automatically, trade by trade — with cost-basis tracking, meaning we follow the purchase price of each position to compute the gain that gets taxed. We also model the ETF no-offset rule we discussed: gains on ETFs are redditi di capitale, and they cannot be reduced by past losses sitting in your loss ledger. That is the world our figures live in. Now, what we do not model. We do not model the regime dichiarativo, where you declare and pay the tax yourself in your tax return rather than having the broker do it. We do not model foreign accounts, which carry their own reporting duties. We do not model the 12.5 percent rate on white-list government bonds beyond a flat approximation — white-list means the roster of states Italy considers cooperative on tax, whose bonds are taxed at 12.5 rather than 26 percent. And we do not model the fine detail of your minusvalenze pregresse — your specific stock of prior realised losses and their expiry dates. So treat every figure here as educational, built on the average Italian retail case, not as a reading of your personal position. Tax rules change; your situation differs from your neighbour's. For anything you would actually act on — above all realising losses on single stocks to offset gains — get a commercialista, an Italian tax accountant, to confirm it in writing first. To be explicit: this is the standard 26 percent regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista. That honesty sets up the last slide: the edge that still survives tax.

The edge that survives tax

So let's close the loop. For a euro-based Italian investor, there is only one edge worth chasing: the edge that survives two things at once — the 26% tax on realised gains, and the euro itself. Everything we measured this episode points the same way. A foreign gross backtest — a strategy that shines in dollars, before tax, before local costs — is a mirage. It is not built for you. The truth for us is a single number: the return net of tax, in euros, after costs, judged over the whole window. That is the number that actually buys something.

So what do we do about it, in practice? Three things, and they run through every engine we build. First, we put the tax inside the objective from the start — the 26% on realised gains is not a footnote we add at the end, it is part of what the model is trying to win. Second, we defer realisations deliberately: a no-trade band that keeps the portfolio still unless a move is worth the tax it triggers, so that unpaid 26% stays invested and keeps compounding for you. Third, we judge every engine on what it keeps, not on what it shows in a brochure — net, across the time blocks, with costs on both legs.

Remember the size of the prize we are defending against: the tax drag we measured was three to four-point-four percentage points a year. That is bigger than almost any published factor, and bigger than a full year of our own research. This is the standard 26% regime amministrato with cost-basis; rules change and individual situations differ — consult a commercialista.

Next episode: the alpha graveyard. The strategies we tested and killed — and the exact numbers that killed them. Because knowing what does not work, honestly, is half the edge. See you there.